KASPI.KZ (LSE:KSPI)

Wonderful Company at Wonderful Price

Kaspi.kz (March, 2022)

The Everything App

1: Overview

As Warren Buffett wrote in his The Security I Like Best article for The Commercial and Financial Chronicle in 1951, “boomtime profits and record dividend payments do not set the stage for depressed security prices.” Kaspi is not a business that is “misunderstood.” I doubt investors have a hard time understanding what Kaspi does and why it does it so well. A simple look at its ~ 85% return on equity, ~ 55% return on invested capital, compounded revenue growth of 27% since 2016, and record margins will show just how good of a business Mr. Lomtadze has built over his 15 years at the helm of the company. Instead, Russia’s recent invasion of Ukraine – as well as the political unrest in Kazakhstan in January – has forced Kaspi back to its IPO price of ~ $34 despite having its earnings almost double since going public. That’s not to say, however, that recent geopolitical and economic developments won’t have an impact on Kaspi’s performance and competitive advantage. For many investors, the spread of potential outcomes is simply too wide to be able to comfortably determine the range of intrinsic value for the company.

2: Core Business

The nature of Kaspi’s Super-app allows for synergies and value creation between its three different segments: Fintech, Marketplace, and Payments. As standalone products, the three divisions are more vulnerable to their respective competitors: Payments to Visa and Mastercard; Fintech to Halyk Bank; and Marketplace to companies like Chocofamily and Yandex.Eats. Combining into one app, however, allows the divisions to drive user growth and traffic for one another. Visa isn’t just competing with Kaspi Payments – it’s competing with the whole range of services that Kaspi offers. What’s more, divisions can essentially acquire a portion of new customers at zero cost thanks to Kaspi’s “customer sharing” ecosystem.

Payments is generally the key driver for user growth, although it accounts for ~ 29% of net income (with Fintech taking up 49% and Marketplace 22%). Like WeChat or Venmo, Payments has naturally attracted users through network effects. I myself, for instance, involuntarily became a user of Kaspi simply because my friends and family used the app. Kaspi’s introducing bill payments into its platform has also added substantial value (although it’s not necessarily a traffic acquirer) and today bill payments are Payment’s second most used product (followed by QR Payments). People can pay taxes, parking tickets, fines, utilities, and other expenses through the app.

In order to attract and retain customers, Kaspi’s P2P transactions are generally fee-free. Hence, although P2P accounts for 76% of total payment volume, it makes up only 9% of revenue generating transactions (QR and Card account for 73% and bill payments for the other 18%). Kaspi can theoretically attempt to monetize P2P transactions more, but given Mr. Lomtadze’s focus on customer satisfaction and product quality that change likely won’t take place. With more users adopting the app (generally for P2P purposes), merchants/ retailers began shifting to Kaspi to capture the growing traffic on the app. Today, Kaspi’s merchants generate an estimated average of 33% of their revenue through the app. Simply put, merchants can’t afford not to sell through Kaspi’s Marketplace, a conclusion supported by the platform’s 99% merchant retention rate. The only way to pay for products on Marketplace is through BNPL from Fintech or using Kaspi Gold from Payments– an example of how different segments generate users and revenue for each other. Fintech is Kaspi’s “original” business (Kaspi used to be “Bank Kaspiysky” founded by Chairman Mr. Kim). Although it doesn’t see the same explosive “catch-up” growth as the other two divisions, Fintech generates 49% of earnings and was crucial as a source of cash flow to grow Payments and Marketplace. Mr. Lomtadze’s decision to just focus on short-term consumer finance products gives the company more flexibility (for example, it managed to quickly taper off lending during COVID) and pricing control.

3: Segment Overview

Payments

Payments is the bread-and-butter of Kaspi. Like with the phrase “Google it,” many in Kazakhstan started using Kaspi as everyday slang – a sign, at least to me, of meaningful share of mind and brand recognition. Kazakhstan never really had a P2P platform before Kaspi, and so users fled onto the app. Within a couple years, Kaspi has managed to get roughly half of Kazakhstan’s population onto its platform.

Few companies can boast displacing Visa and Mastercard from their dominant market share within a year (Kaspi’s share is roughly 70% today). Using QR-codes also allowed merchants to skip the need to acquire costly third-party POS terminals. Walking in the Green Bazaar (a local landmark and one of the largest markets in Almaty), one could see that every wall is plastered with the respective Kaspi QR-codes of merchants. People often don’t even bring cash with themselves anymore. In terms of business, Kaspi’s TPV (Total Payment Value) was 50.5 trillion KZT (~ $100 billion) and revenue-generating TPV was 12.9 trillion KZT (~ $30 billion). Average TPV take rate was 1.2% (around 1.1-1.3% historically), with the majority of revenue-generating volume coming from Kaspi QR/Card. RTPV increased almost 8-fold since 2018 as more merchants began accepting Kaspi QR. Gross margins are around ~ 88% (85% in ‘20, 76% in ‘19, and 69% in ‘18), and – given the small fixed costs of operating the platform – margins could very well be in the low-mid 90s within a few years.

An extract from the 2020 Annual Report:

Kaspi.kz Payments Platform is the largest driving force behind Kazakhstan’s transformation from cash to cashless and digital transactions. Based on NBK data, our TPV corresponded to a market share of 69% in 2020 for total cashless and digital transactions (card payments, P2P payments, internet and mobile payments) effected in Kazakhstan, up from 65% in 2019.

What’s more, Kaspi Payments (like other divisions) has expanded over time to target merchants as well. For instance, it sent out Kaspi Pay POS terminals to retailers for free, seeing an explosion of its merchant base. It charges ~ 2.3% for all cards (including Kaspi Gold) and 0.95% for QR payments. Today, Kaspi’s QR is the most popular method of payment in Kazakhstan.

What ended up happening was, in essence, a cycle of user and merchant attraction: the more users use the platform, the more merchants are incentivized and encouraged to switch over to Kaspi which, in turn, makes Kaspi a more attractive payment option for customers. With its own POS terminals, Kaspi now has control over both sides of its transactions.

Another fascinating example of Kaspi’s ability to successfully introduce new products is Kaspi Gold, which today is one of the most used cards in Kazakhstan. Customers go to “Kaspi Kartomats” and get their own card, with their initials, printed right in front of them within 60 seconds. Kaspi now offers Smart POS, mobile QR, and QR Display for its merchants – all shipped, maintained, and manufactured by Kaspi for free. Kaspi’s entering the B2B Payments market should drive further merchant usage as companies start using the platform to pay for supplies and send payments.

In 2016, around 161 billion KZT in payments was made digitally. By June 2021, almost 6.3 trillion KZT payments were digital – a 39-fold increase. Kazakhstan remains one of the leading countries in terms of payment digitalization, with total digital payment value increasing 138% in 2021 vs. just 39% in Russia. Today, over 77% of all transactions are digital. This is a rare case where a company triggers change, not the other way around. Kaspi didn’t just “ride the wave” of digitization and benefit from the shift to digital payments: it was the very thing that brought around this change.

Payments, in my eyes, is also incredibly resilient when it comes to both local and international competition. The payment processing market is, in many ways, a winner-takes-all environment where network effects essentially magnify whatever product the majority of customers decide to adopt. With its dominant market share and an already-defeated Visa and Mastercard (I don’t see how they can match Kaspi’s convenience and quality), much of the competitive threat remains local. Russian companies won’t be entering anytime soon – and Kazakhstan is too small of a market for some of the larger players who have poor knowledge of the country.

Mr. Lomtadze success with Kaspi has drawn many envious stares, and several well-established companies and businessmen are trying to develop their own form of Kaspi. Onai, a national bus-card company which has started turning its popular Onai application and bus cards into a payments platform, is one of the more promising competitors. They already have millions of users on its platform (every person using bus as transportation uses Onai) and have a history of successful product implementation. Unlike Visa and Mastercard, which fail to cater to the needs of the demographic, these companies have deep expertise on the local industry and consumer trends/ behavior. Another one is Choco, a company that has replicated many of Kaspi’s products (Marketplace, Payments, etc.) but, for some reason, never thought of combining all of its services – which are of fairly high quality – into one ecosystem like Kaspi. A large strategic blunder in my opinion. So yes, there are companies out there that have good products, but Kaspi’s growing market share, mixed with its competitive advantages and its ecosystem structure, keep me optimistic about the division's future.

Marketplace

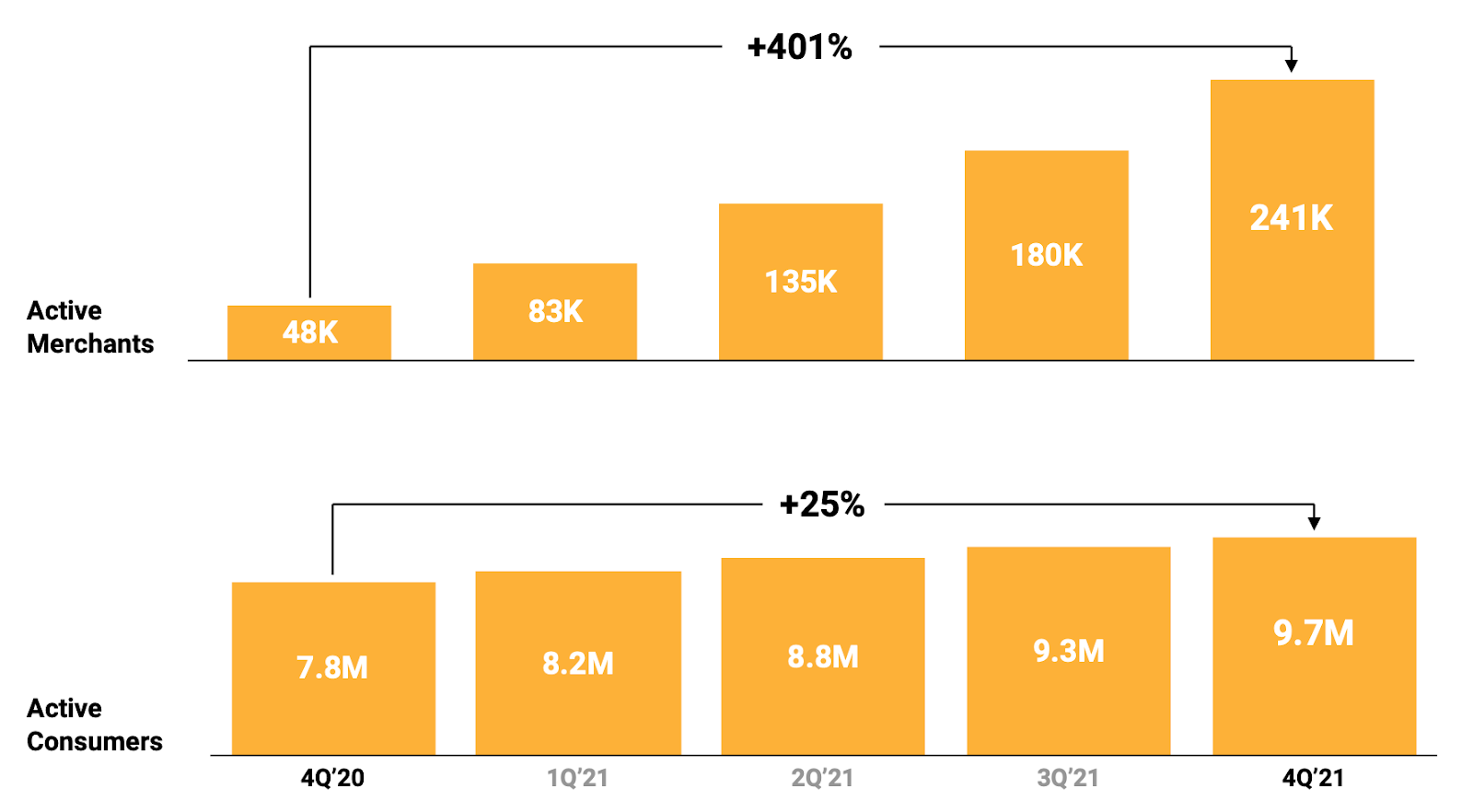

Kaspi’s Marketplace revenue increased 2.3 times year-over-year to $355mm and GMV increased 2.2 times to KZT 1.8 trillion. GMV take-rate improved from 5-6% in 2017 and 2018 to 8.5% this year. GMV has grown at a compounded growth rate of ~ 47% since 2016. Latest Q4 merchant count is up to 122k, up almost 3-fold from 32k last year. Since more merchants are shifting to accepting Kaspi/ using Kaspi’s POS terminals, they also start listing/ partnering with Kaspi’s marketplace platform. As previously mentioned, Kaspi estimates that retailers make ⅓ of their revenue through the platform. With the every-day consumer using Kaspi for payments, Marketplace essentially gets a large portion of its traffic at no cost. Third-party retailers come and list their products on Kaspi, where consumers then choose the product they want and then from which retailer they want to buy (3P – Alibaba). Kaspi should also start ramping up marketing/ traffic options like Aibaba where 3P sellers pay for performance.

The company recently developed its own “Postomat” product which essentially serves as a delivery locker. Postomat accounts for ~ 5% of all deliveries in Almaty, although (at least from my experience) customers still aren’t used to the product and prefer to do in-store pickup or delivery. Mobile-commerce still accounts for the majority of GMV ~ 63%, and will likely continue to make up the bulk of GMV as customers prefer to buy in-store. That, quite frankly, is the issue with e-commerce (at least for now). Delivery companies like Yandex.Eats and Glovo (think Uber Eats and Doordash) have just recently become widely-used/ accepted. People still aren’t used to ordering/ buying things online, and many still find it easier to just go and buy whatever they need at the local supermarket or electronics store. This could be another story, like with Payments, where Kaspi drives the change, but there is 1) significantly more competition and 2) more complex implementation that makes it hard to successfully replicate Payments’ success.

It also recently entered the e-grocery delivery market with Magnum’s dark stores (one of Kazakhstan’s oldest and largest supermarkets). I doubt e-grocery will lead to any meaningful revenue (that is, however, not to say that it won’t grow.) Mom-and-pop grocery/ convenience stores are scattered all across major cities and are, in a way, ingrained into local culture. Since Soviet times, it was common for each “rayon” or district/ neighborhood to have their small grocery stores which people would go to. Magnum doesn’t have the scale or the product quality to separate itself from these stores. If, however, Kaspi manages to get these small grocery stores onto the platform, it can very well dominate the whole grocery market in Kazakhstan. Moreover, companies like Glovo already have a meaningful market share and well-established logistics, making it harder for Kaspi to break into the market.

Another issue with Kaspi’s Marketplace is the lack of a robust delivery/ fulfillment infrastructure. Kaspi still relies fairly heavily on outside logistics and delivery services to help it with its fulfillment; although it works well now, with orders usually arriving within a day if you live in the city, increasing traffic requires further investment in logistics. Moreover, although Kaspi indicates one-day delivery, there are often times when traffic is too high and deliveries get postponed. Even a one day delay could result in Kaspi permanently losing a customer.

Unlike Payments, Marketplace faces significant competition. From Tatyana Belkachuk’s Wildberries (which in many ways could be considered superior) to AliExpress and Mechta.kz, the ecommerce market is, in my opinion, overcrowded and lacks the needed barriers to entry. Moreover, unlike Payment's network effect and share of mind, Marketplace is, to some extent, a commodity-like service. Customer’s don’t care who they buy from, especially since the products listed are from generic retailers. Going forward, I hope Kaspi can attract actual brands (like with Alibaba’s Taobao) as currently most sales come from every-day electronics, beauty products, and clothes. The fact, however, that Marketplace managed to grow as much over time speaks to the effectiveness of Kaspi’s ecosystem to attract and “share” customers. Mr. Lomtadze has done well in keeping Kaspi’s Marketplace as strictly a service/ platform business (hence the ~ 93% gross margin). Since Kaspi neither manufactures nor warehouses the products (as the retailers essentially act as warehouses), it does not need to invest as much, enjoys higher margins, and gets to scale the business cheaper and easier. Kaspi’s reputation and very active user base (MAU to DAU is an astounding 54% with only WeChat higher at 92%) also make it a no-brainer platform for merchants. Moreover, Marketplace generates a substantial portion of Fintech's BNPL product.

Fintech

Fintech used to be what Bank Kaspiyskiy was all about. After acquiring the bank in 2002, Mr. Kim realized that banking wasn’t something where he could replicate the success of his Planeta Elektroniki business (one of the largest household electronics retailers at the time). Kazakhstan had been an independent country for around 10 years by then, and many entrepreneurs were moving into the promising yet overcrowded banking sector. Then came Baring Vostok. Under Michael Calvey, Baring (with Mr. Lomtadze as partner) took an equal stake in Kaspi after Mr. Kim bought out his partner in 2006. More about the company could be read in Harvard Business School’s case study of Kaspi.

Kaspi managed to leverage its Super-app ecosystem, as well as its in-house algorithms, to gain an edge over its competitors (most notably Halyk Bank). What’s more, Lomtadze simplified operations to focus on the short-term consumer credit market. This shift allowed the company to gain flexibility in pricing and size of financing, as well as reduce cost of risk. For instance, the company managed to scale down lending/ origination during COVID, and scale it back quickly once the macro improved. Total Finance Volume (TFV) more than doubled in one year to 4.3 trillion KZT with a much higher conversion rate of 2.4x. Average net loan portfolio increased 72% to 2.3T, while yield decreased to 28.6% due to a shift in deposits/ loans makeup.

Halyk, in terms of total assets, is larger than Kaspi due its other operations outside of consumer credit (KZT 12T in assets vs. Kaspi’s KZT 3.6T. However, Kaspi has the dominant market share in consumer loans (32% vs Halyk’s 18%) and higher digitalization (100% for Kaspi vs. 59% for Halyk). Customer experience is also superior – Kaspi can lend out money within a couple minutes while Halyk may take as long as a week. I can see Kaspi expanding more aggressively into the SME finance market as well with its merchant Super-app, and I think it can once again displace Halyk as the market leader.

BNPL is still the majority of TFV, and unlike loans and deposits (which grow naturally in line with the industry and benefit from additional cross-division users), gets to ride along with the explosive growth of Marketplace. Business finance should also grow into a larger share of total TFV as merchants continue to shift to the marchant Super-app.

Fintech is a slower growing but more stable source of cash flow for the company. Non-performing loans ratio decreased to 4.7% and cost of risk was down to 1.6%. Once again, unlike traditional banks, Fintech benefits from the ecosystem’s sharing of customers.

The cherry on top of this is the roughly $6.4 billion in customer deposits or float that the company then gets to invest in (predominantly) bonds. Given Kaspi’s history of introducing new products, I wouldn’t be surprised if they implemented something like insurance onto the platform (think of all the float!!!). Kaspi did have an insurance operation before called “Basel”, but it ended up selling it to an undisclosed 3rd party. I think insurance makes sense and compliments the Fintech product portfolio. Since Kaspi also started growing its car finance business, insurance seems to be a way of tacking on growth (sort of like with BNPL).

4: Moat

We’ve already talked about some of the more obvious moats of the company, which are predominantly its structural advantages and Payment’s network effect. Kaspi’s ecosystem makes it hard for any individual company/ product to offer the same level of value. Even if consumers might get better rates or prices elsewhere, many choose to use Kaspi simply because of the convenience and reputation of the brand. With its network effects, Kaspi can just spit out quality services onto its platform and have them gain millions of users within a year. Take Kaspi Travel for example. After introducing the product in 2021, Travel’s GMV grew almost 20x in just one year and the number of tickets sold increased over 28-fold. It would be hard to find another company that gains such a large number of users in such a short period of time at virtually no cost. To some extent, there is already a “built-in” advantage for any product Kaspi releases into its ecosystem.

One of Kaspi’s main competitive advantages, however, is its focus on customer satisfaction. If one listened to any of Mr. Lomtadze’s interviews or read his letters, they would constantly come across the phrase “our dearest customers.” That, in a nutshell, is what Kaspi is about: delivering quality services to make its customers’ lives easier. In an interview on the Kazakhstan Growth Forum 2021, Mr. Lomtadze explained that “[Kaspi has] no rules or borders around our products – we just want to make lives better.” And make their lives better they have. No product or service offers as much value as the Kaspi’s Super-app, and the range of services just keeps growing every year. A commonly shared statistic by the company is its net promoter score – a metric for customer experience/ satisfaction. The NPS used to stay below 40% in the early 2010s. Now, NPS is 87% and increasing. People genuinely love Kaspi – they love how easy it is to use their products, how accessible they are, and how convenient it is to have everything packed into just one app. Management has a long-term, customer-driven approach that prioritizes product quality and user experience over immediate profits. In the same interview, when asked about how he will stay on top of competition, Mr. Lomtadze explained that “each company has to know what its competitive advantage is, and continually invest in that competitive edge.” His continuous investments into further improving service quality and value of services lead to, in the long-term, expansion of Kaspi’s competitive advantage. Customers may love Kaspi now, but they’ll love it even more in the future.

Another overlooked advantage of Kaspi, in my view, is its R&D capabilities. The company has a fabulous track record of coming up with high-quality services in-house and effectively introducing them into the market. From the face-recognition technology to its lending algorithms and POS terminals, everything Kaspi has is – contrary to popular belief – developed within the company. Take Kaspi Pay POS terminals. After growing its user base and erasing the need for terminals with its QR code, Kaspi set out on an aggressive merchant-acquisition spree. It created a market for merchants where POS Terminals were no longer a viable solution, and then implemented the very thing it disrupted for free to all of its customers. Today, 82% of all transactions are processed through Kaspi Pay. From Postomat to Kaspi Travel, e-grocery, Kaspi Gold, and B2B Payments, Kaspi has an established track record of developing superior products within a matter of months (many of its products have been developed within 6 months) and then successfully introducing them to the market. Mr. Lomtadze, when asked about the threat of outside competition, replied: “People think that Russian or other international countries have some ‘out of this world’ skill and talent that we here in Kazakhstan lack. People think the companies will come and just start pushing us out of the market. Well, I say this: let them come. We will welcome them, don’t worry.” Like with Amazon, such R&D capabilities are hard to replicate and remain, in my eyes, one of the most significant sustainable advantages of the company.

5: Management

Mr. Lomtadze has won PWC’s CEO Of The Year for 5 years in a row. He loves what he does, and sees Kaspi as his own unique creation. Lomtadze has been at the company since 2006 and took over in 2007, so in many ways he has built the company from the ground up. His philosophy of customer-obsession at all cost is something that really separates him from his competitors. Mr. Lomtadze has also talked extensively on his focus to maximize the company’s talent pool through in-house teaching and a selective process of recruitment. In 2021, the company introduced Kaspi Labs which offers courses in data science, java, and .net development. Last year, out of the 7000-8000 people that went through the whole process, only 150 got accepted – an acceptance rate of just ~ 2% (who said something about Harvard?) In Kazakhstan, IT specialists are a hot commodity and the government has set a goal of training 100,000 specialists within the next 5-10 years. Kaspi, then, is sitting on a gold mine of talent compared to many of its competitors. I truly believe (and definitely hope) that Mr. Lomtadze is in it for the long-run, and almost all of his net worth is in the company.

Management owns over 50% of outstanding shares and, given the recent decline in stock price, I expect a hefty share buyback within a few months. During the rebuilding phase of the company, Mr. Kim and Mr. Lomtadze essentially fired all of management (most of whom were bankers and financial experts) and replaced them with, predominantly, computer science and software specialists. According to Mr. Lomtadze, the company’s culture shifted to an environment that allowed for innovation and creativity. Dress code, for instance, changed from formal business suits to casual t-shirts and jeans. Lomtadze claims that employees and management love what they do and do it with a passion – knowing that their products are “improving lives of their dear clients.” In one of his interviews, he stated that “we don’t set some unattainable financial goal for the next five years and work towards reaching it. Instead, we sit down and think – say, some people need help registering their car. We then go and create something in 6 months that will help them register it.”

6: Risks

It is, first of all, important to note how Kaspi reacted during the January unrest in Kazakhstan. There are videos on Telegram of terrorist-seized armored vehicles literally smashinig into Kaspi’s ATM buildinig and another video of marauders breaking Kaspi’s ATM and taking out all of its cash. Over 20 of Kaspi buildings were attacked in one way or another. There were gun-shots and dead bodies outside of our apartment. During the crisis, Kaspi acted with confidence in 1) making Kaspi work without access to the internet as network connections across the country were down and 2) created a “News” feed for people to keep updates on what’s happening. 60 thousand people would use its “News” segment every hour. Kaspi worked closely with Kazakhstan's ministry of digitalization to help make Kaspi available 24/7 despite the lack of network connection.

Since the unrest in January, President Tokayev has replaced virtually all ministers and high-ranking government officials. Kaspi has also fallen into the “good graces'' of the government: a poster child of the sort of innovation Kazakhstan is capable of, and a crucial talking point in attracting foreign investments. Kaspi’s Gov services (taxes, bills, checks, child aid, etc) were created based on Kaspi’s continuous working with the government. The services are largely free and, as of today, Kaspi Government is larger than the government created eGov app that offers similar services.

Now onto Russia. Kazakhstan’s economy, whether we like it or not, is tied to Russia’s. It is a crucial economic partner and Kazakhstan is heavily dependent on Russia’s economic wellbeing. The Kazakh government refused, however, to recognize Donetsk and Lugansk as regions independent of Ukraine, and abstained from voting on the conflict (granted, abstaining isn’t exactly rejecting but it is a radical change from previous approaches to international relations.) Kazakhstan today is a refugee corridor for Ukrainiins fleeing to this side of the world. Being so dependent on Russia, however, means that there are implied currency risks. With current sanctions, it seems overly optimistic to think that Kazakhstan’s economy is not going to be affected.

As long-term business-owners, however, we try to abstain from making any geopolitical and macro projections. Despite the high probability (and I would say a virtual certainty) that Kazakhstan’s economy is going to be hit in the short term, I remain cautiously optimistic (and obviously to some extent biased) about the political and economic future of the country.

7: Valuation

Trying to project earnings or free cash flow of a company that has grown at ~ 27% since 2016 is, in my view, a wasteful way to spend your time and an inaccurate way to think about the business. With ~ $380mm in net cash, $6.4b in customer deposits, 85% ROE, and 55% ROIC, ~ $1b in earnings, and $1.4b in securities, current levels of valuation, whatever way you look at it, are absolutely absurd. At a market cap of $7-8b, Kaspi is trading at a ~ 12.5% earnings yield. We, essentially, get all future growth for free. A conservative valuation of ~ $80-90 can be made as a “bear” case assuming Kazakhstan’s economy is hit harder than expected. Companies like PayPal, despite a large decline, are still trading in the low 20s EV/EBITDA. Kaspi, in the long-term, remains a quality business run by quality people yet today is trading like a no-growth commodity-like company, and that’s not even considering the ~ 6-7% dividend yield.

In a recent interview, Mr. Lomtadze mentioned that “for every one service, we already have three others in our head that we’re waiting to implement.” Kaspi has a long runway of high-quality products that, as we have seen with Travel, need limited capital and a short amount of time to grow to substantial proportions. What’s more, demographics across the CIS are relatively uniform. Kaspi has already entered Azerbaijan with some classifieds acquisitions and Ukraine (although it is to be seen how that investment will play out). Total CIS population is roughly 80mm, and in many cases the countries lack a platform like Kaspi. All of the countries speak Russian – after all, we were all part of one country not too long ago. The economics of the Super-app also allow for cheap and easy implementation. Kaspi doesn’t need to invest in building a factory or getting the needed equipment. It can scale at very low cost. Moreover, there’s nothing about Kaspi that makes it solely a “Kazakh” company. Its CEO is Georgian, and the company is named after the Caspian sea (bordering Azerbaijan, Turkmenistan, Iran, etc.). Its products could easily be implemented internationally with virtually no change. As Sir John Templeton said – “the point of maximum pessimism is the best time to buy.” It is hard to think of a more pessimistic outlook regarding our side of the world than today.

Great work Ilya. The company's extensive focus on customers really reminds me of Amazon and the way Bezos ran the company with customers in mind rather than competitors. I just wonder weather you see the ecosystem around Kaspi as a win,win ecosystem, focusing on alignment with merchants and partners? as according to Ron Adner is the reason behind the succes of Amazon Marketplace.

Great write-up. Thanks llya. I kind of made Kaspi go viral through a note or maybe other way around, it made me go viral. It had 37k impressions, 500 subs, simply nuts. Here is the note: https://substack.com/@diyinvestor1/note/c -92984431?r=4ukla6